-

A Macro Lull

-

Demand: Starting As Expected

-

Supply: Mispriced

The unofficial start to the summer buying season is March because it’s the first month when a buyer could go under contract and realistically achieve a summer move. From here, we expect a pick-up in demand through the end of July in which prices historically accelerate rapidly. Given that mortgage rates are back above seven percent, and the average price of a sold home in the Denver metro is up over 40% since 2019, it will be interesting to see if we get the same price action over the next few months. We believe the market will hit a high plateau in which low supply keeps prices elevated and the average person feels pricing is very expensive. Indeed, we believe that we are approaching that point quickly as last month was the first month (outside of May 2020…) when the average price of a sold home in Denver was down year-over-year in over eight years. This is significant because the average list price of a home is up 11% as of the end of the month – something will definitely have to give.

A Macro Lull

We rang the bell last month as it related to Silicon Valley Bank and what we believe is an ongoing credit crunch. The equity markets shrugged off this bad news as a result of implicit support from the US government, though, the bond market is suggesting that something is still very “weird.” The 2-year note hit a yield-high of 5.1% in March before rallying to ~3.6% and now settling in around 4.0% – these moves are literally unprecedented and suggest a strain on the system.

This graph above is from the St. Louis Fed and shows the percentage of lenders who are tightening standards for both large/mid (blue) and small (red) businesses. What was surprising to us is that even before the SVB fallout in Q1 2023, banks had been tightening standards for a couple of quarters. If you review the data going back to 1992, there are three other times in which standards have tightened this much: 2000-2001, 2008-2009, and 2020. Unlike those other periods of time, this time very unique because the Federal Reserve is currently fighting inflation which will make it very, very difficult for them to flood the system with additional liquidity should the economy falter.

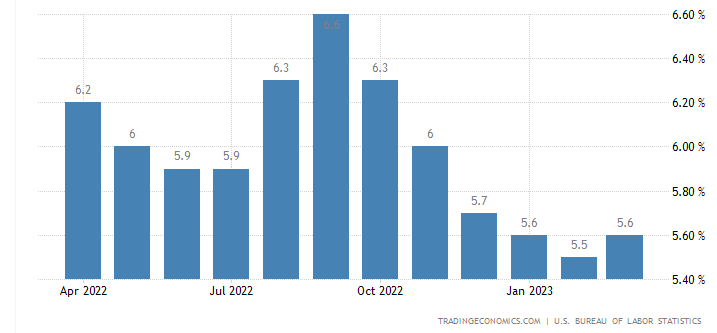

Turning to inflation... Core inflation data as measured by CPI and PCE are still running above the committee’s 2.0% target and are tracking between 4-6% depending on your preferred metric. Core CPI came out this week and even showed a tick-up in the annual inflation readings:

The Fed is consistently saying they are not going to be done raising rates until there are “real rates across the curve.” If the 2-year note is at 4% and inflation is running above 5% (real rates equal nominal rates minus inflation), then they aren’t cutting anytime soon… Additionally, with 10-year rates at 3.5%, they don’t have much wiggle room to deviate from their implied 2% inflation target without truly jeopardizing our long-term yield curve; the result of losing the back of the curve would be way worse for our economy than slightly misjudging to the hawkish side right now.

We feel the Fed has to err on the side of raising rates until they are sure inflation is near their 2% target which means rates are still going to go up. The cost of a mortgage is probably closer to the low end of the range right now, and that suggests that our housing market likely has a bit further to cool before heating up again when all of this inflation stuff is over.

Demand: Starting As Expected

Let’s check in on our trusty table summarizing the current conditions in Denver’s housing market within a 10-mile radius around downtown:

(All data taken from REColorado from April 7-12, 2023)

Demand is starting off as expected: picking up versus earlier in the season and still lighter than what it was at this time last year. The reason for the slow start is that rates are up another 1.5-2% versus last year while list prices are up another 10% on average. As a result, the cost of purchasing a home increased by over 15% from the previous year, and it seems that buyers are running out of purchasing power.

This is evident based on two data points: Days on Market (DOM) and Avg Sold YoY. The medium DOM for listings in our market dropped from 30 days in January to 7 as of March – that means that homes were taking a month to put under contract two months ago while now it’s only expected to take a week. This is a change that suggests demand is coming back into the market and taking all available supply. At the same time, however, the average price of a sold home DROPPED 4.5% versus last year which is only one of two months this has happened since the Fall of 2014; the other time was May 2020, which almost doesn’t count.

The market typically appreciates significantly more when there’s this little supply available. For example, last March had a DOM of 4 (yes, four days) and we saw price appreciation of over 20% versus March 2021; March 2019 was at 11 DOM and still appreciated over 5% vs. March 2018. The fact that the average price of a sold home is going down while the market is very tight is one of the clearest signs we’ve seen that buyers are maxing out their purchasing power.

Supply: Mispriced

When I say “mispriced,” I don’t mean the market is inefficient and there are arbitrage or investment opportunities – in fact, we think it’s quite the opposite. It appears that the average listing in the Denver metro area is going on the market now assuming that buyer demand will be just the same as always during this point in the buying season and buyers have extra pockets of cash they can use to put toward affordability. This is definitely not the case.

As you can see on the two columns from the right on our chart, list prices have projected double-digit increases in average sales prices going back the entire year and have been “wrong” for the last 10 months. Whether it’s remote work ending, less affordability (higher rates and prices), or just “waiting until a better time,” sellers have seemingly been going on the market and expecting too much. The lack of supply would normally suggest that sellers are able to get their asking prices, but something is off.

With prevailing interest rates and an average sold price of $750k, the average home in Denver costs ~$5,500/month to carry including principal, interest, taxes, and insurance. That means your household has to make approximately $180,000 per year in income (without any other outstanding debt service) to afford the average sold home in the Denver metro area. The US Census Bureau estimates that the median income in Denver in 2021 was approximately $80,000, and even providing for substantial increases in salary, it would be impossible for the average person to buy the average home in Denver right now.

This distortion was made worse during the pandemic as we had a lot of immigrants (mostly domestic) who had a lot of cash or were downsizing from more expensive areas to Denver. Now that the demand from these heavy-cash buyers seems to be gone and the usual underwriting standards are putting a cap on what can be paid in the metro area, it appears that affordability is going to be the main issue when trying to achieve current list prices.

Increasing Affordability

Our team understands that affordability is the name of the game right now, and that’s why we are very, very excited to make an announcement on April 18th that will help our clients afford between 5-10% more on every purchase – at no cost to the buyer. Please, sign up for our mailing list or reach out to someone on our team to find out how you can get this benefit, too!